Compelling question

How have economic policies after Reconstruction, and the Great Depression, and today contributed to the wealth gap between ethnic groups in the United States?

Reading Questions:

How have economic policies after Reconstruction, and the Great Depression, and today contributed to the wealth gap between ethnic groups in the United States?

Reading Questions:

- What was the Freedman’t Bank and what happened to it?

- Why was HUD created?

- What is Redlining? Why did the Federal Government begin Redlining?

- How did Redlining affect wealth, education, and health in the different areas?

- How did Redlining affect the value of homes in the different areas?

- How did the Great Recession of 2007-2009 affect people of color?

The Freedman's Bank

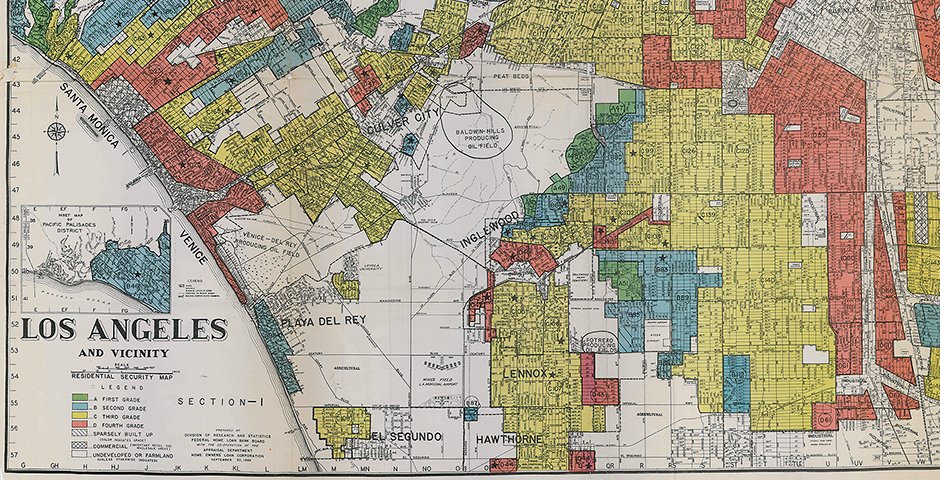

Redlining

|

During the Great Depression, many banks failed causing a drastic decrease in home ownership in the US. In the 1930’s the US was faced with a housing crisis. Roosevelts New Deal created the Federal Housing Administration (HUD). They created a program where the Federal government would ensure private bank loans for people. Since the loan was insured by the government, the bank could give people loans with low-interest rates.

The Federal Housing Administration contributed to segregation efforts by refusing to insure mortgages in and near African-American neighborhoods — a policy known as "redlining." At the same time, the FHA was subsidizing builders who were mass-producing entire subdivisions for whites — with the requirement that none of the homes be sold to African-Americans. African-Americans and other people of color were left out of the new suburban communities — and pushed instead into urban housing projects.

|

Redlining also included the federal government creating maps for realtors. These maps "graded" neighborhoods into four categories, based in large part on their racial makeup. Neighborhoods with minority occupants were marked in red — hence "redlining — and considered high-risk for mortgage lenders.

African Americans also faced discrimination in lending practices. Banks were less likely to lend to people of color. When given loans, people of color paid higher interest rates. Fewer loans meant fewer housing opportunities for all people of color.

African Americans also faced discrimination in lending practices. Banks were less likely to lend to people of color. When given loans, people of color paid higher interest rates. Fewer loans meant fewer housing opportunities for all people of color.

Long Term Impacts

Wealth

As a result of redlining, families of color did not have access to the same generational wealth. The housing in the neighborhoods that excluded African Americans increased in value. Parents were thus able to pass on the houses or equity to their children creating generational wealth. The state-mandated segregation led to less housing thus fewer economic opportunities for African American families and families of color.

Health

As a result people of color ended up living in the city while whites lived in the suburbs. To this day, people of color are more likely to live near industrial plants that produce toxic waste. Additionally, people of color in the city are less likely to live in places where the water is not drinkable as evidence by the incident in Flint Michigan in 2018. Moreover, people of color are more likely to live in housing with unhealthy conditions like toxic paint or lead. This results in people of color having higher instances of cancer and asthma.

Education

Redlining also had an affect on people's education. The main way the schools get funding is through property taxes. People in neighborhoods with more expensive homes have better funded schools with more resources. In turn, the better the schools the more the homes are worth. The higher the values of homes, the more taxes they have to give to the schools creating a cycle.

As a result of redlining, families of color did not have access to the same generational wealth. The housing in the neighborhoods that excluded African Americans increased in value. Parents were thus able to pass on the houses or equity to their children creating generational wealth. The state-mandated segregation led to less housing thus fewer economic opportunities for African American families and families of color.

Health

As a result people of color ended up living in the city while whites lived in the suburbs. To this day, people of color are more likely to live near industrial plants that produce toxic waste. Additionally, people of color in the city are less likely to live in places where the water is not drinkable as evidence by the incident in Flint Michigan in 2018. Moreover, people of color are more likely to live in housing with unhealthy conditions like toxic paint or lead. This results in people of color having higher instances of cancer and asthma.

Education

Redlining also had an affect on people's education. The main way the schools get funding is through property taxes. People in neighborhoods with more expensive homes have better funded schools with more resources. In turn, the better the schools the more the homes are worth. The higher the values of homes, the more taxes they have to give to the schools creating a cycle.

Sub Prime Loans and the 2008 Crisis

In 1995 Clinton loosened bank regulations from the Great Depression including housing rules by rewriting the Community Reinvestment Act, which allowed banks to lend in low-income neighborhoods. Most of the loans in the low income neighborhoods included subprime loans. Those are loans with higher interest rates. This action would eventually had to the 2007-2008 Recession. The recession, while painful for everyone, was especially disastrous for black Americans. Prior to the crash, the median wealth for a white household excluding a home was $92,950. For blacks that figure was $14,200. When factoring in home equity, the wealth of black households grew more than four-and-a-half times, to $63,060. For white households factoring in home equity helped wealth figures grow by only about two-and-a-half times to 244,000. Department of Treasury which found that black families and Latino families living in upper-income neighborhoods were two times more likely than white households in lower-income neighborhoods to have refinanced their homes with subprime loans. The report also notes that black and Latino households were nearly 50 percent more likely to face foreclosure than their white counterparts. Thus the recession hit minority families much harder than white families, adding to the already existing wealth gap.